Credit Spread Explained: Stunning Guide to the Best.

Article Structure

In both cases, the core idea is the same. You take on risk in exchange for a higher potential reward. Understanding credit spreads helps investors judge risk, compare investments, and build more resilient portfolios.

Credit Spread: Short Definition

In finance, the term “credit spread” has two common meanings. Context matters. One relates to bonds and loans. The other relates to options trading.

- Bond credit spread: The difference in yield between a risky bond and a safer benchmark bond.

- Options credit spread: An options strategy where you sell one option and buy another, collecting net premium (a “credit”).

Both uses point to the trade-off between risk and compensation. In bonds, you earn extra yield for default risk. In options, you earn premium for taking market risk within defined limits.

Credit Spread in Bonds and Fixed Income

In bond markets, a credit spread shows how much extra yield investors demand to hold a bond that might default, compared with a safer bond that is very unlikely to default. The safer bond is often a government bond from a stable country.

For example, suppose a 5-year government bond yields 3%. A 5-year corporate bond from a weaker issuer yields 5.2%. The credit spread is 2.2 percentage points, or 220 basis points.

How to Calculate a Bond Credit Spread

The calculation is straightforward. You compare two securities with similar maturity dates but different credit quality.

- Find the yield of the risky bond (for example, a corporate or high-yield bond).

- Find the yield of a reference bond with similar maturity (often a government bond).

- Subtract the reference yield from the risky bond’s yield.

If a corporate bond yields 6.5% and a government bond with the same maturity yields 4.0%, the credit spread is 2.5% or 250 basis points. This spread reflects extra compensation for default risk, liquidity risk, and sometimes sector or country risk.

What Changes a Bond Credit Spread?

Credit spreads move all the time. They widen or tighten based on how investors see risk. Several forces drive these moves.

- Company health: Better earnings, lower debt, and strong cash flow often lead to tighter spreads.

- Economic outlook: In recessions or stress periods, investors demand higher spreads, especially for weaker issuers.

- Market liquidity: If trading dries up, buyers require more yield, so spreads widen.

- Interest rate level: While spreads are about credit, big shifts in base rates can affect how investors view risk across assets.

As a simple scenario, imagine a retailer with heavy debt. If news shows a sharp drop in consumer spending, investors may worry about defaults. The retailer’s bond spread can jump from 200 to 450 basis points in a few days as investors demand more yield to hold that risk.

Credit Spread in Options Trading

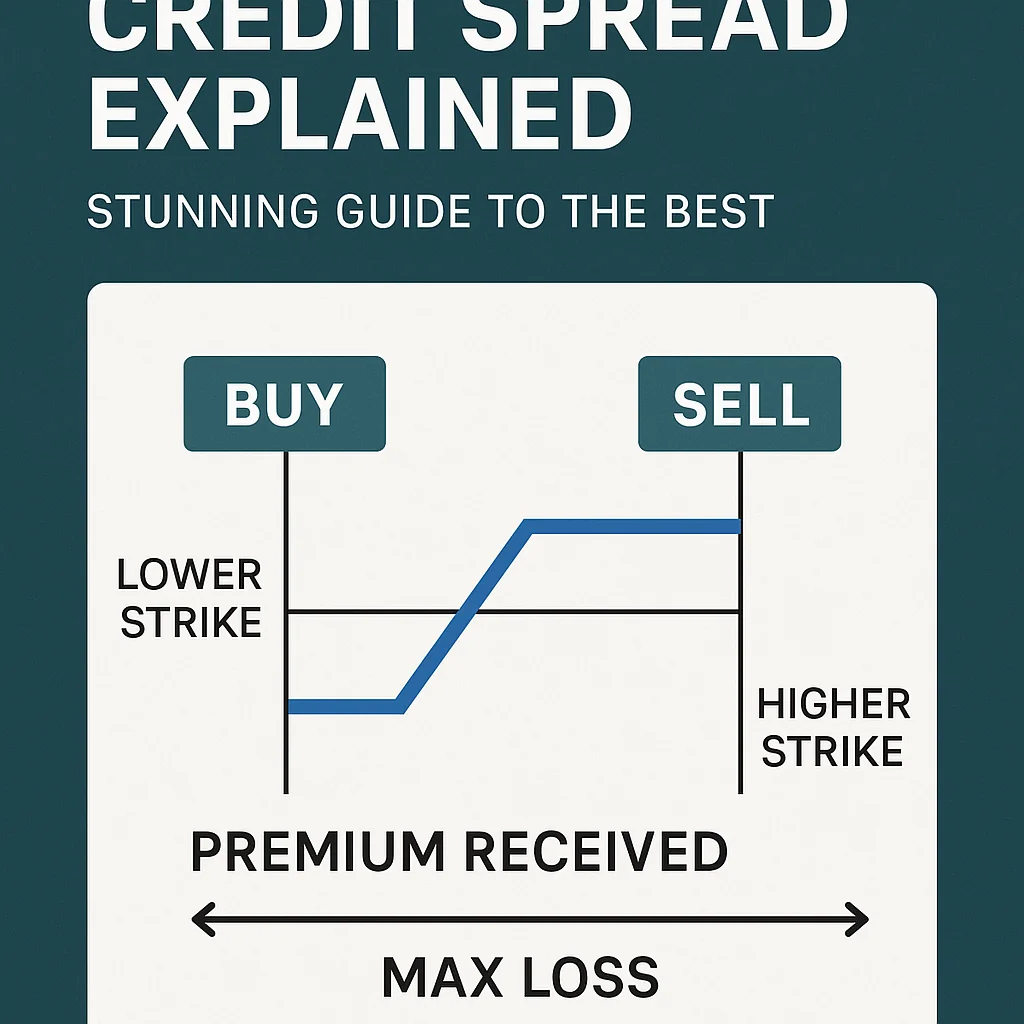

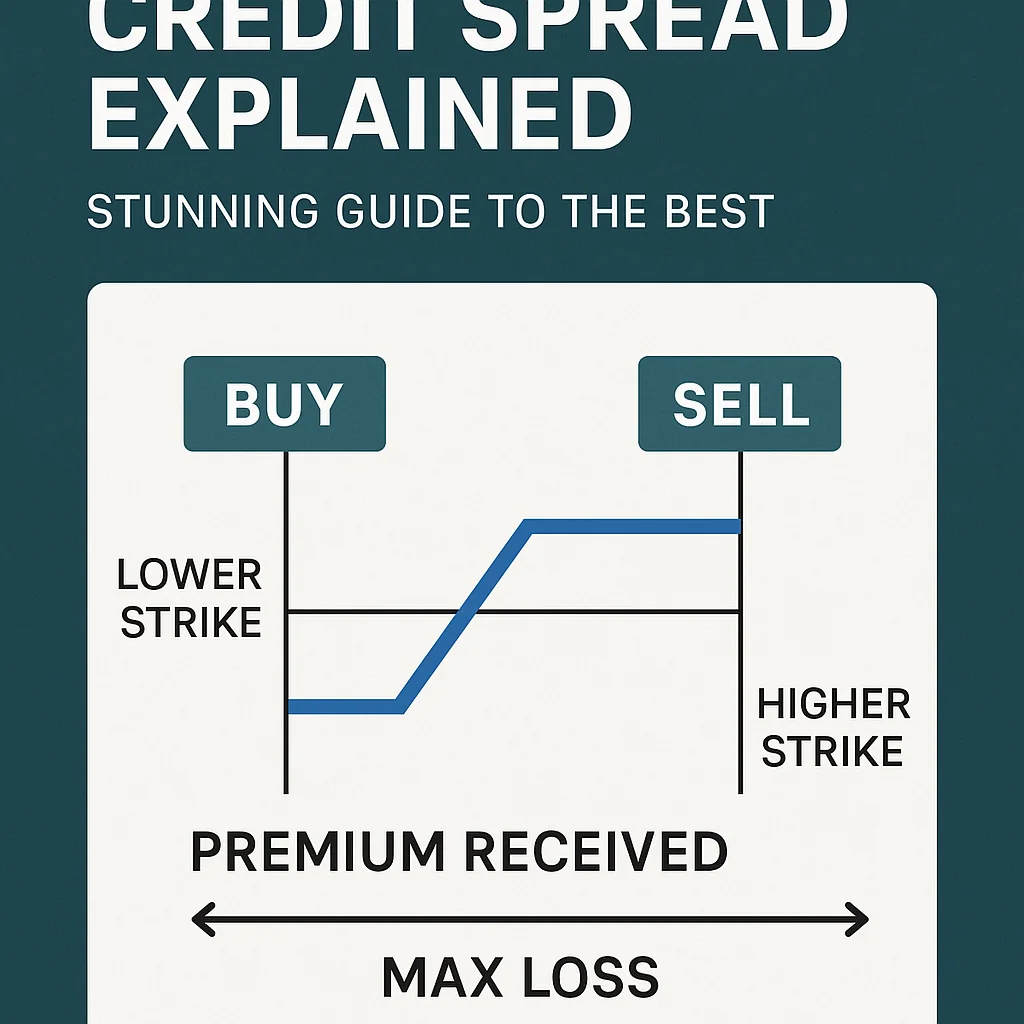

In options markets, a credit spread is a strategy that generates net premium at the start. Traders sell an option with a higher premium and buy another option with a lower premium on the same underlying asset and with the same expiration.

The trade creates a defined maximum loss and a capped maximum profit. The net credit (the premium received) is the most the trader can earn if conditions move in the desired direction or stay within a certain range.

Types of Options Credit Spreads

Most credit spreads use calls or puts with different strike prices. Here are common structures:

- Bear call spread: Sell a call at a lower strike, buy a call at a higher strike. You profit if the price stays below the short call strike or falls.

- Bull put spread: Sell a put at a higher strike, buy a put at a lower strike. You profit if the price stays above the short put strike or rises.

- Iron condor (combination): A combination of a bear call spread and a bull put spread. It collects credit from both sides and profits if the price stays within a set range.

Each structure defines risk by pairing a sold option with a protective bought option. The result is limited downside and limited upside, built around the initial credit.

How an Options Credit Spread Works: Simple Example

Imagine a stock trades at $100. A trader expects the price to stay above $95 over the next month but does not want to buy the stock. They create a bull put spread:

- Sell a $95 put for $4.

- Buy a $90 put for $2.

- Net credit received = $2 (4 − 2).

Here the maximum profit is $2 per share, which occurs if the stock finishes above $95 and both options expire worthless. The maximum loss is $3 per share: the $5 wide strikes minus the $2 credit. The credit spread lets the trader express a moderate bullish view with capped risk and limited profit.

Key Differences: Bond vs. Options Credit Spreads

The same phrase covers two different ideas. A short side-by-side view helps keep them clear.

| Aspect | Bond Credit Spread | Options Credit Spread |

|---|---|---|

| What it is | Yield difference between risky and safe bonds | Strategy with sold and bought options that brings in net premium |

| Main focus | Default and credit risk | Price movement and volatility risk |

| Investor role | Passive holder of bond income | Active trader managing positions and expiry |

| Reward source | Higher yield over time | Premium collected upfront |

| Risk limit | Potential loss if issuer defaults or sells off sharply | Maximum loss defined by strike distance minus net credit |

Both uses involve taking a credit risk of some kind. In bonds, the risk is the issuer’s ability to pay. In options, the risk is the asset price moving beyond the range that the spread can handle.

Why Credit Spreads Matter to Investors

Credit spreads help investors make sense of risk and reward. They act as a quick signal of stress in individual securities and across markets.

- Risk pricing: Wider credit spreads often indicate higher perceived risk.

- Market sentiment: Sharp, broad spread widening can signal fear or expected economic weakness.

- Portfolio construction: Spreads help balance income needs against tolerance for loss.

- Timing decisions: Some investors increase risk when spreads are wide and trim risk when spreads are very tight.

For example, many long-term investors track average spreads on high-yield (“junk”) bonds. Very tight spreads can hint that investors are relaxed and maybe ignoring risk. Very wide spreads can show distress but also may offer higher future returns for those who can withstand volatility.

Risks Linked to Credit Spreads

Credit spreads offer higher return potential, but they also come with real risks. Ignoring these can lead to sudden, large losses.

Risks for Bond Investors

Bond credit spreads depend on credit quality and the economic cycle. Several risks stand out:

- Default risk: The issuer may miss interest payments or fail to repay principal.

- Downgrade risk: Rating agencies may cut the issuer’s rating, causing spreads to jump.

- Spread widening risk: Even without default, the bond price can drop if investors demand more yield.

- Liquidity risk: In stress, it can become hard to sell a bond at a fair price.

An investor who bought a bond with a 200 basis point spread might see it jump to 600 basis points during a crisis. The bond price can plunge even if the company survives, which hurts if the investor needs to sell before maturity.

Risks for Options Traders Using Credit Spreads

Options credit spreads define maximum loss, but they do not remove risk. Key issues include:

- Gap risk: The underlying asset can jump through both strikes overnight.

- Assignment risk: The short option can be exercised early by the buyer.

- Margin calls: Large swings can trigger margin requirements and forced adjustments.

- Volatility shifts: Rapid changes in implied volatility can move spread prices sharply before expiry.

A trader who sells many small credit spreads for modest income can be hit hard by one sharp move. The sum of limited losses can still be large if position size is aggressive.

How Investors Use Credit Spreads in Practice

Credit spreads are not just abstract numbers. They play a central role in day-to-day decisions.

- Bond selection: Income-focused investors compare credit spreads across issuers and sectors to find attractive risk-adjusted yield.

- Economic signals: Asset allocators watch spreads for early warnings of stress or recovery.

- Hedging: Institutions may buy or sell credit default swaps (CDS) to manage exposure, which are priced mainly from credit spreads.

- Income strategies with options: Options traders use credit spreads to seek steady premium with controlled downside.

Consider a conservative investor who wants higher income than government bonds but cannot accept large drawdowns. They might hold a mix of investment-grade bonds with moderate spreads and a small slice of high-yield bonds with larger spreads. At the same time, an options trader might sell credit spreads on broad indices, collecting premium while capping losses with protective legs.

Reading and Using Credit Spreads Wisely

A credit spread, in bonds or options, is a clear expression of the trade-off between extra return and extra risk. Wider spreads signal more risk and more potential reward; tighter spreads suggest less risk but lower compensation.

Investors who respect what credit spreads reveal can make sharper choices. They can compare bonds more clearly, judge market conditions with more context, and, for those who trade options, build strategies that define risk upfront. The key is simple: understand what the spread pays you for, and decide if that payment is enough for the risk you are taking.